Galleon Insider Trading Charges

The US Justice Department and the US SEC filed insider trading complaints against the billionaire Raj Rajaratnam, his Galleon hedge fund and several other friends and associates a few days ago. All the interesting stuff (for example, the transcripts of telephone conversations) are in the criminal complaints filed by the Justice Department. If one reads only the SEC complaint, one would not realize that there are several smoking guns here.

The fact that the whole thing was made possible by the FBI’s use of informants and wiretaps appears to provide some support for a controversial paper by Peter Henning posted at SSRN last month. In this paper, titled “Should the SEC spin off the enforcement division?,” Henning argued that “To allow the SEC to regulate Wall Street properly, splitting off at least a portion of the enforcement function to an agency with expertise in prosecutions – the United States Department of Justice – is at least worthy of consideration as the government looks to increase regulation.”

One reason why the Department of Justice had all the advantages here is that insider trading is very simple to understand. There is no need for a PhD in finance to recognize insider trading if the prosecutors have access to all the communications that are taking place. But absent such access, insider trading is notoriously difficult to prove. So here, wiretapping expertise beats finance expertise hollow.

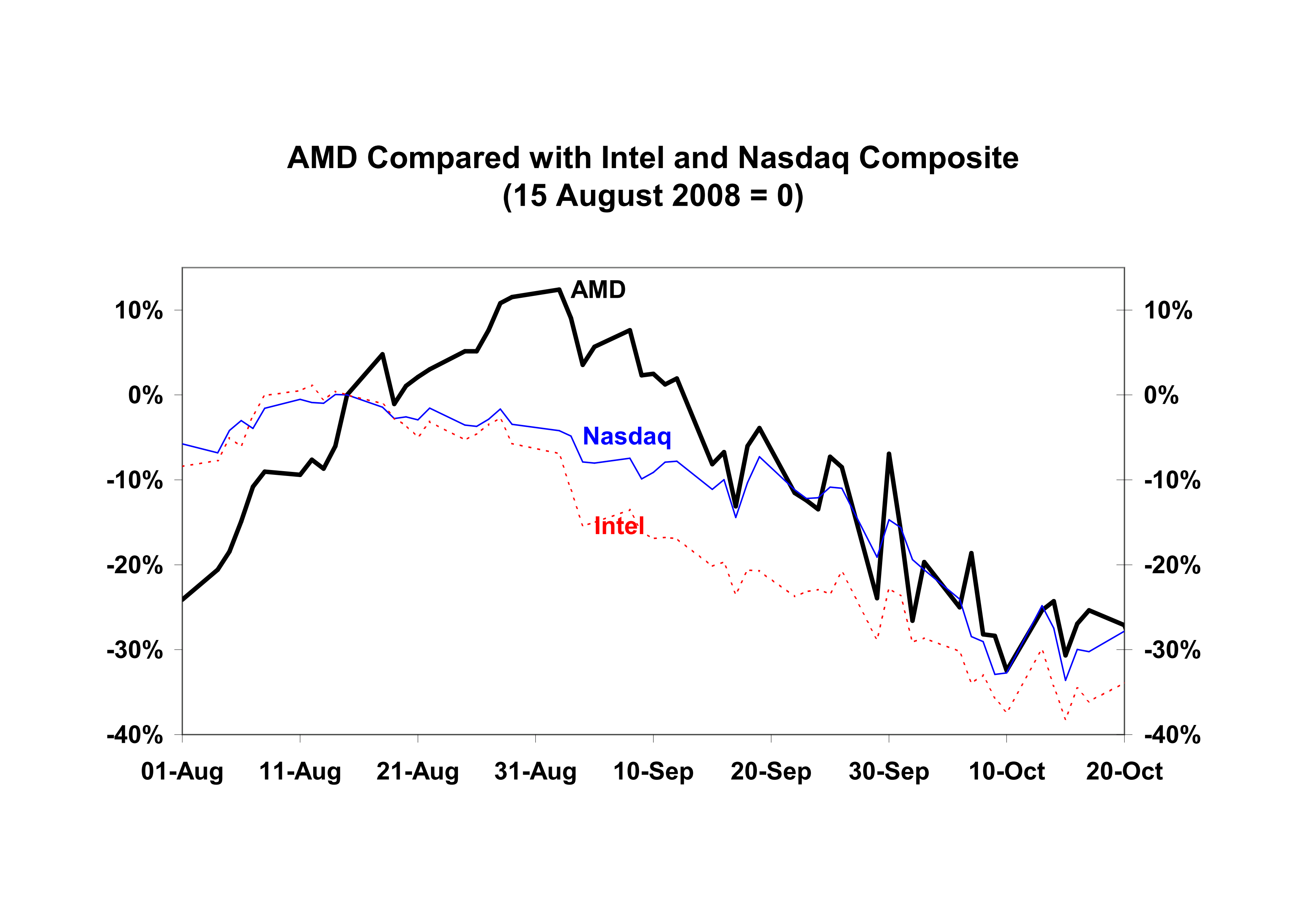

At another level, it was interesting to find that with all the insider information that they had from multiple sources, the defendants lost money trading AMD shares prior to its announcement of the spin off of the fabrication facilities and a capital infusion by Abu Dhabi. The complaint attributes it to a general decline in stock prices due to the global financial crisis. The defendants bought AMD stock beginning August 15, 2008, the Lehman collapse occurred in mid September, the AMD announcement happened on October 7, 2008 and the defendants sold stocks around October 20, 2008.

But the global financial crisis is not the whole story as seen from the graph below. Even if the defendants had hedged their AMD long position with a short position in the Nasdaq Composite index, they would not have made money. Yes, AMD does outperform Intel over the period, but not by a huge amount.

It appears from the graph that around the time that the defendants were buying AMD on inside information, many others were also buying. They could also have been buying on inside information or on pure rumours. The graph reminds me of the old adage: “buy the rumour, sell the fact.” It is also possible that the Abu Dhabi deal was not as attractive as people initially thought and the prices reacted to this reassessment. In other words, if Galleon had the advantage of superior information, other traders might have had the advantage of superior analysis. The complaint contains the transcript of a telephone conversation where two defendants agree on a division of labour: one of them is to collect the information and the other is to analyze it. The second person probably was not up to the task.

Posted at 4:45 pm IST on Wed, 21 Oct 2009 permanent link

Categories: insider trading, investigation

Comments