India in a ZIRP world

I wrote a column in the Financial Express today about why Indian interest rates need to come down much more when the world interest rate is going down to zero.

While discussing the magnitude of interest rate cuts in India – the RBI cut repo rate and reverse repo rate by 100 basis points each and CRR by 50 basis points on Friday – we need to remember that the entire developed world appears to be converging to a zero interest rate policy (ZIRP). This is a completely unprecedented situation and points to interest rates much lower than what we are accustomed to seeing.

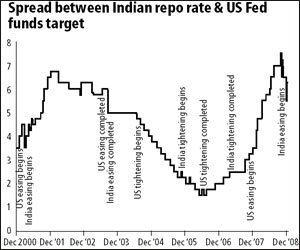

India is an open economy and even the capital account is quite open for all practical purposes. Indian interest rate policies are therefore strongly influenced by global interest rate. A comparison of the Indian repo rate and the US Fed Funds Target since 2000 shows that Indian tightening and easing follows US tightening and easing with a lag. Essentially, an open economy forces the RBI to follow what the “world central bank” does; and the only flexibility that it has is to delay its response by a few months.

Now, the US has pushed its interest rate down to virtually zero. Japan has also done the same, and the European Central Bank is also being dragged down that path much against its wishes by the sheer strength of global forces. In that situation, how low should Indian interest rates go?

The plot above shows the spread between the Indian repo rate and the US Fed Funds target with key tightening and easing episodes demarcated on it. Because of the lag between US and Indian central banks, this spread fluctuates a lot.

For example, in July 2006, the US had completed its tightening cycle and India was still half way through its tightening cycle. The spread between the two rates fell to an abnormally low level of 1½% with the Fed Funds target at 5¼% and the Indian repo rate at 6¾%. Over the next nine months, India tightened by another 1% to 7¾% while the US rate remained unchanged at 5¼%. In April 2007, with both central banks having completed their tightening cycles, the spread was 2½% which can be regarded as a “natural” spread between the rates in the two countries reflecting differences in the respective inflation rates and other structural characteristics of the two economies.

In September 2007, the US began easing interest rates in response to the financial crisis. At that time, the crisis in the US appeared very remote to us, and India left rates unchanged for several months. Then earlier this year, the RBI raised interest rates by 1¼% to 9% in response to the inflation scare which gripped the country at that time. The spread between US and Indian rates rose to an extraordinary level of 7½% in October 2008.

Since then, India has been easing more sharply than the US and the spread came down to 6½% by the end of 2008. But this is still a very high spread. If we consider the April 2007 spread level of 2½% as a “natural” spread, then the Indian repo rate needs to come down to well below 3%.

That is a much steeper cut than what RBI has made. But even that might be an underestimate of what would be needed. The US has gone beyond zero interest rates to a regime of quantitative easing which pushes long rates down to low levels. Since it is not possible to make interest rates negative, quantitative easing achieves the same effect of negative interest rates by expanding the balance sheet of the central bank.

This means that to achieve the same spread against the “effective” (quantitative easing adjusted) interest rate in the US, Indian rates would have to come down even more. Similarly, European interest rates are lower than what they appear to be because the expansion of the ECB balance sheet has some of the characteristics of quantitative easing.

I believe that the RBI should cut its interest rates very rapidly to a level consistent with global interest rates for four reasons. First, the prospect of further cuts in rates in future makes long term government bonds a one way bet – they are today the most attractive asset for any bank on a risk adjusted basis. There is no point exhorting banks to lend when the central bank rewards “lazy banking” through the gradualism of its interest rate policy.

Second, India can afford a fiscal stimulus only if interest rates have first been brought down to very low levels. Otherwise, the weak fiscal capacity of the state is wasted on paying an excessive interest rate on its borrowings.

Third, the weakening of the currency caused by low interest rates is a stimulus that the economy needs very badly.

Finally, since many economists now project inflation at 2% or so by the end of this fiscal year, steep rate cuts are needed to prevent real interest rates from becoming excessive.

Posted at 7:50 am IST on Sat, 3 Jan 2009 permanent link

Categories: crisis, monetary policy

Comments