Indian exchanges must go regional and then global

Indian stock exchanges are now confronted with an urgent need to look beyond the borders of India and formulate a vision for their role in the Asian stock exchange business. When I wrote about this last year (FE, November 30, 2010), I thought that Indian exchanges might have a year or so to get their act together. Global consolidation in the exchange space has moved much faster in the last few weeks and this timeframe has shrunk dramatically.

Last year, the Singapore exchange (SGX) initiated the process of consolidation in Asia with a bid for the Australian exchange (ASX). Though this bid appeared to have stalled, it is now receiving an uplift from a wave of global consolidation. The London Stock Exchange (LSE) wants to merge with the Canadian exchange (TMX) to create a transatlantic platform for listing and trading equities. This plan is dwarfed by an even more ambitious proposal by the German exchange Deutsche Börse (DB) to merge with NYSE Euronext to create a behemoth in equities and derivatives trading.

It is now clear that exchange consolidation is not going to be on a regional scale. Increasingly, the goal will be to create exchanges that span several continents and provide a single platform for trading stocks and derivatives from all over the world round-the-clock. In a year or two, when the LSE-TMX and DB-NYSE combines have completed the integration of their respective mergers, they will be looking at acquiring Asian exchanges to complete their global reach. Many analysts now believe that 5-10 years from now, there will probably be 4-5 global exchanges, each of which spans Asia, Europe and the Americas.

At that point, the Indian exchanges will have the choice between splendid isolation (and irrelevance) in a globalised world and becoming a relatively minor piece in a global exchange. To avoid this fate, Indian exchanges need to act now to spearhead the formation of pan-Asian exchanges that would have much greater bargaining power during the final round of consolidation.

There are two reasons for optimism that Indian exchanges can play a key role in the first phase of Asian consolidation. First, India is a large and fast growing emerging market. Second, Indian exchanges are world-class in terms of market design, range of derivative products, large and varied investor base, sound regulation and high liquidity.

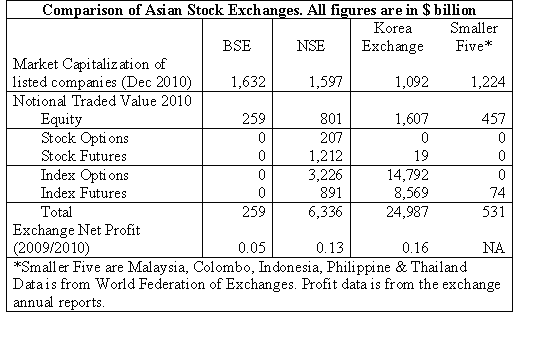

If we exclude developed markets like Japan, Australia and Singapore, and if we regard China, Hong Kong and possibly Taiwan as being in a class of their own, then India and Korea are the emerging markets of the Asia-Pacific region, with large and vibrant equity and derivative markets. Korea has the world’s largest index derivative market while India is the premier market for single stock futures.

The accompanying table compares Indian and Korean exchanges with the aggregate of other Asia-Pacific emerging markets to demonstrate how large these two countries loom over the rest.

A partnership of some form (an alliance, if not a merger) between the Korean and Indian exchanges would clearly be a formidable Asian exchange that could, over time, absorb other smaller Asian exchanges and introduce derivative markets in those countries. Just as Euronext (a merger of European exchanges) subsequently became a major part of a transatlantic merger, it is easy to visualise this pan-Asian exchange becoming a significant part of a global exchange in the final phase of global consolidation towards the end of this decade.

Of course, any such alliance would involve tricky issues of valuation.

For instance, the Indian market capitalisation is 1½ times that of Korea; Korean traded value is nearly 4 times that of India; the exchange profit numbers are comparable; and the long-run growth prospects are probably better in India.

When it comes to regulation, nothing much will change because each exchange as a separate operating subsidiary could continue to be regulated by its current national regulator. Any merger would, however, require changes in national regulation on foreign shareholding and other related matters.

Needless to say, the purpose of this article is not to campaign for a specific merger or alliance. The purpose rather is to illustrate, with sufficient particularity, the thought processes that Indian exchanges need to go through in identifying potential partners and working out various permutations and combinations in order to derive the maximum possible advantage for themselves and for India.

Posted at 11:16 am IST on Wed, 23 Feb 2011 permanent link

Categories: exchanges

Comments