We assume ...

The Basel Committee on Banking Supervision (BCBS) issued a Consultative Document on "Revisions to the Basel Securitisation Framework" earlier this month. Under "Key assumptions and theoretical underpinnings", I found this gem:

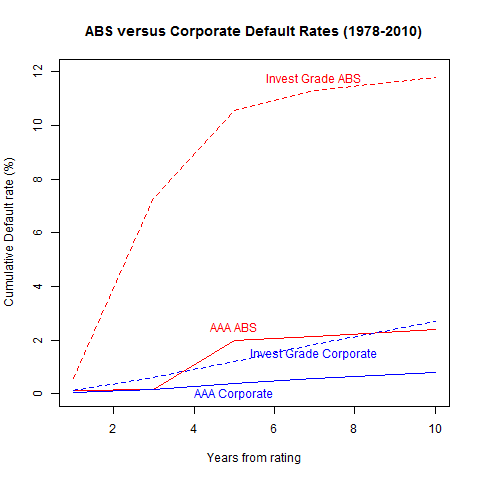

Another important assumption embedded in the RBA recalibration is that the same ratings for structured finance and corporate exposures imply the same expected loss rates for investors. One implication of this is that it is assumed that rating agencies will “fix” or have fixed the errors in rating methodologies for structured finance that were revealed during the recent crisis.

Just to put that assumption in perspective, the plot below shows the difference in default rate over the last three decades (and not just during the crisis) between Asset Backed Securities (ABS) or structured finance and corporate paper with the same ratings. The source for the underlying data is Standard and Poor’s via a recent paper by Gorton and Metrick (Table 8) that I hope to blog about soon.

I used to make the assumption that the regulators will “fix” or have fixed the errors in regulatory capital calculation methodologies for structured finance that were revealed during the recent crisis. That assumption must now be abandoned.

Posted at 10:01 pm IST on Sat, 29 Dec 2012 permanent link

Categories: credit rating

Comments